Wealth tips & tricks

The Importance of Emergency Funds in Your Financial Freedom Journey

10 mins

May 27, 2025

Wealth tips & tricks

10 mins

May 27, 2025

Financial freedom means different things to different people. For some, it might mean being able to take care of their family's needs without any financial stress, ensuring they can provide for necessities like housing, education, and healthcare without worrying about the costs. For others, it might mean having the ability to make aspirational purchases, such as luxury items or experiences, without considering the price tag.

Whatever one's personal goals may be, financial freedom is about having the financial security to cover your essential needs, which then allows you to pursue your wants and dreams without financial constraints. It provides peace of mind and the ability to make choices that enhance your quality of life, whether that’s through supporting loved ones, investing in personal growth, or simply enjoying life’s pleasures

So how do you pursue that? Simple, by building an emergency fund.

An emergency fund helps you navigate life's unpredictabilities, such as job loss, health issues, and unexpected bills. An emergency fund is basically six months of your salary, but it can be more, depending on how much you are willing to save in a given period of time. The key idea behind building an emergency fund is principal protection and not wealth creation.

According to a survey by the personal finance platform Finology, 75% of Indians do not have emergency funds and could default on their equated monthly instalments (EMIs) if they suddenly lose their jobs. This can lead to stress from accumulating EMIs and their interests. In some cases households have had to sell properties to cover medical expenses. While emergencies cannot be prevented, having an emergency fund allows you to overcome them.

Here’s how you build one:

From the daily icecream to the occasional night out, every single paisa that you spend should be accounted for. Why? Knowing your money is growing your money. Keeping an account of every rupee you spend will help you track your expenses better and if you’re too occupied to do it, download a personal finance manager app like the axio app.

Tracking your expenses will help you understand your needs and wants better and in turn will help you prepare your budget.

Like mentioned, financial goals are different for everyone, it is better to jot them down and try to put a timestamp as to when you’d be able to achieve them. It is easier if you divide them into short-term and long-term goals. Your short-term goals could be to buy a car, or revamp the house furniture, while your long-term goals could be planning to get inflation adjusted income after your retirement, looking after your kids’ education, and their marriage. Deciding on your financial goals in advance helps you be sorted with how you’re going to build your emergency fund.

Having a budget helps you get an idea of what your expenses are and helps you determine the amount of money you’d be able to save depending on what your expenditures are. While doing so, separate your essential expenses (rent, utility bills, fuel, food) from your non-essential ones (eating out, luxury items, unused TV channels).

You might not realise but debts can snag a major chunk of your income, and reducing them helps you have more money at hand. Having more money at hand means you’d be able to build your emergency fund faster.

Once you start relying on your needs, you’d find that you are saving a lot of money. Find ways to stay within your means, relook at your budget, find where you can cut costs, in order to get more savings. However, there is a fine line between compromising and sacrificing, make sure you compromise rather than sacrifice. The aim here is to live a regular life minus the extras.

The goal of an emergency fund is to protect your principal rather than grow wealth. Once you understand your expenditures and how much money you're saving, it's better to keep this fund separate from your spending account. Consider options like a recurring deposit, liquid funds, or fixed deposits (FDs). These options keep your money safe and secure, allow it to grow, and ensure you can access it quickly when needed.

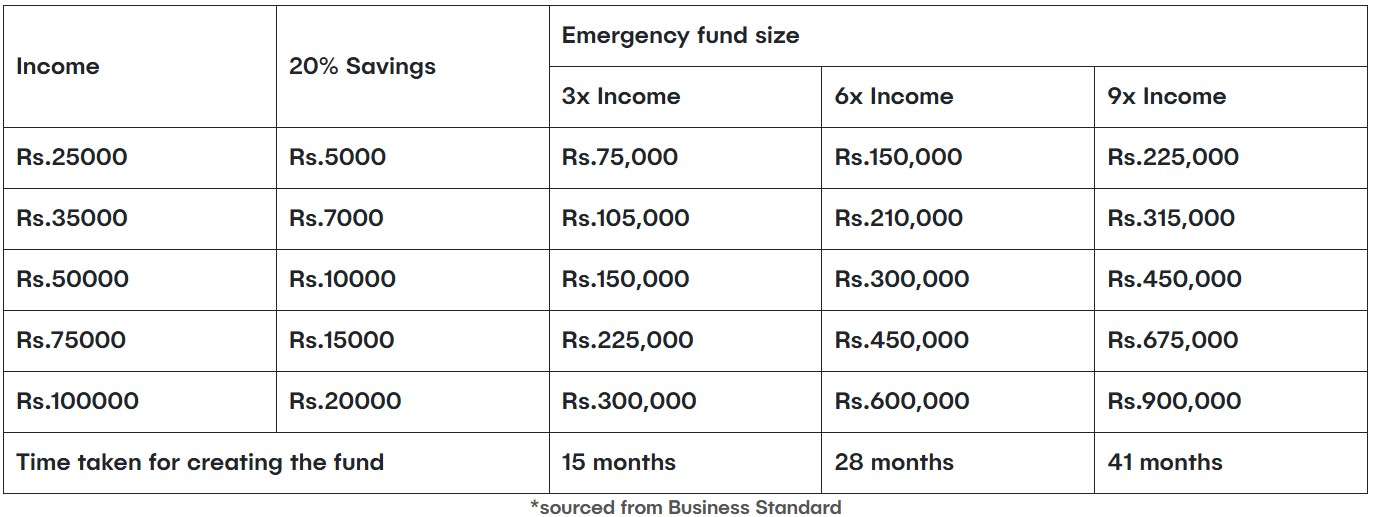

According to Bankbazaar it takes 15 months to create an emergency fund that is equivalent to 3x your monthly salary. Here’s a table* that can help you get a rough idea of the time it takes to create an emergency fund based on income:

However, you’ll also have to take into account the interest you earn and the tax you’ll pay, as mentioned above, this table is just to give you an idea about the time it takes to build the desired emergency fund.

An emergency fund is the first step to becoming financially free, your emergency fund should be untouched, unless something really pressing comes on your way in life. Starting a financially independent future is something that requires years of patience and discipline and like the old adage, it is not easy but it is worth it.

How long does it take to build an emergency fund?

According to Bankbazaar, it typically takes about 15 months to create an emergency fund equivalent to three times your monthly salary, assuming you save 20% of your income consistently. This timeframe can vary based on your saving rate and investment returns.

Can I use my emergency fund for non-emergency expenses?

No, your emergency fund should only be used for genuine emergencies. Using it for non-emergency expenses can deplete your savings and leave you vulnerable during actual emergencies.

Where should I keep my emergency fund?

Your emergency fund should be easily accessible, so consider keeping it in a high-yield savings account, a money market account, or a short-term fixed deposit. Avoid investing it in stocks or long-term investments that can be volatile or difficult to liquidate quickly.

How do I balance saving for an emergency fund with other financial goals?

Prioritise building your emergency fund before tackling other financial goals. Once your emergency fund is in place, you can allocate resources towards other goals like retirement savings, paying off debt, or making significant purchases.

What if I have no savings at all?

Start small. Begin by saving a small percentage of your income and gradually increase it as you get more comfortable with budgeting and saving. Even a small emergency fund is better than none, and over time, it will grow to provide you with more security.

Disclaimer: The information in this article is compiled from various sources and is not to be taken as a substitute for professional advice on managing finances, reader discretion is advised.

.svg)

.svg)

axio (formerly known as Capital Float, Walnut & Walnut 369) is the brand name of CapFloat Financial Services Private Limited, an NBFC registered with the RBI.

© 2025 axio. All rights reserved