Financial Awareness

Filing Income Tax Returns

15 mins

May 27, 2025

Financial Awareness

15 mins

May 27, 2025

Income tax is a noun and it means tax that is levied directly on one’s income—says Google; however, it is deeper than that. Did you know that paying income tax is both a financial and legal obligation? Failure to pay taxes or report one’s income can result in fines and penalties.

According to the Times of India, in 2021-22, ₹4.3 lakh crore of tax was collected. Let’s dive into the numbers. There are 20.9 million taxpayers, compared to an adult population of 943.5 million. Out of those 20.9 million taxpayers, 97 percent fall into the category of paying tax up to ₹10 lakh, while the remaining three percent pay tax above ₹10 lakh. This small segment of individuals contributed to 47.6 percent of the total tax collected.

Comparatively, in countries like the USA, more than 50% of voters are taxpayers. In France, 78.3 percent of voters are taxpayers, 61.3 percent in Germany, and 59.7 percent in the UK. This further cements the fact that the development of a country directly depends on the percentage of people paying taxes. Unfortunately, this percentage is very low in India.

This brings us to the question: if such a small population pays income tax, what are Income Tax Returns (ITRs)? Let’s have a look.

What is an ITR?

For the year 2023-2024, 8.18 crore Indians filed their Income Tax Returns, which is much higher than the number of taxpayers mentioned above. Why is that so? Because when you file an ITR, you declare all sources of income, which may include salary, business profits, rental income, interest on investments, and any other earnings.

Additionally, you must report eligible deductions and exemptions that can reduce your taxable income, such as contributions to retirement savings, health insurance premiums, and certain charitable donations.

The purpose of filing an ITR goes beyond compliance; it ensures transparency in financial dealings and helps the government track the flow of income within the economy. It also plays a pivotal role in enabling taxpayers to claim refunds. In situations where the tax deducted at source (TDS) or advance tax payments exceed the actual tax liability, the excess amount is refunded to the taxpayer by the Income Tax Department.

Overall, the Income Tax Return is a vital tool for both the government and taxpayers, ensuring that tax processes are fair, transparent, and efficient.

How to file your ITR?

Follow these steps to file your ITR

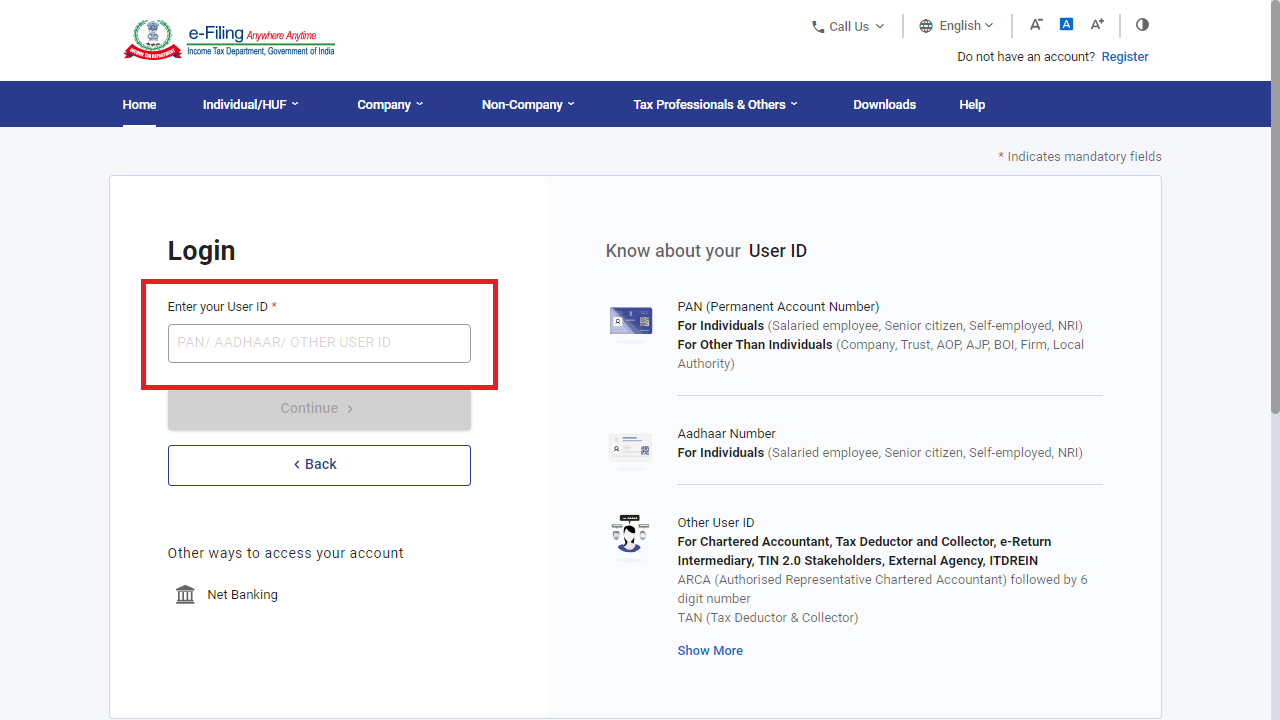

*Make sure that your PAN is linked with your Aadhaar.

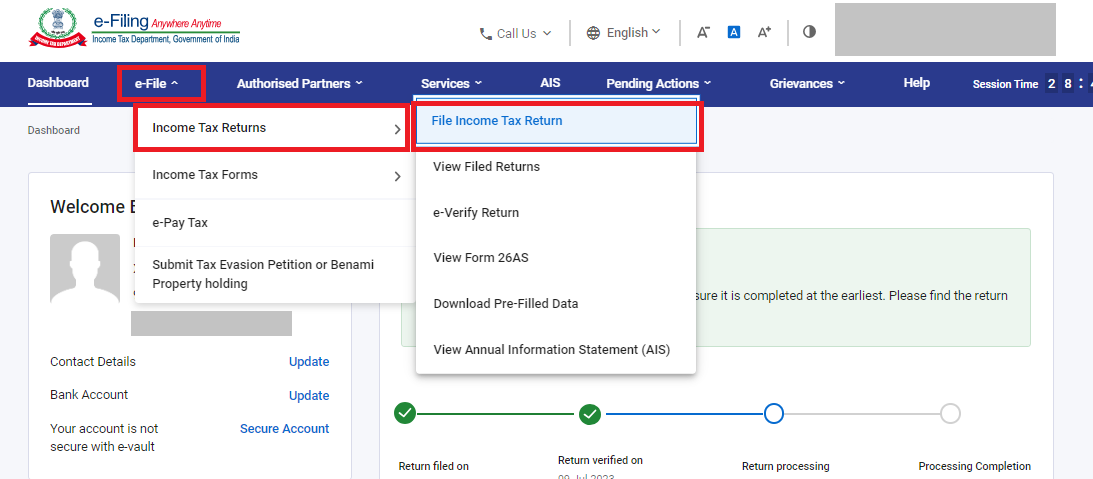

After logging in click on the 'e-File' tab, select 'Income Tax Returns' select ‘File Income Tax Return’

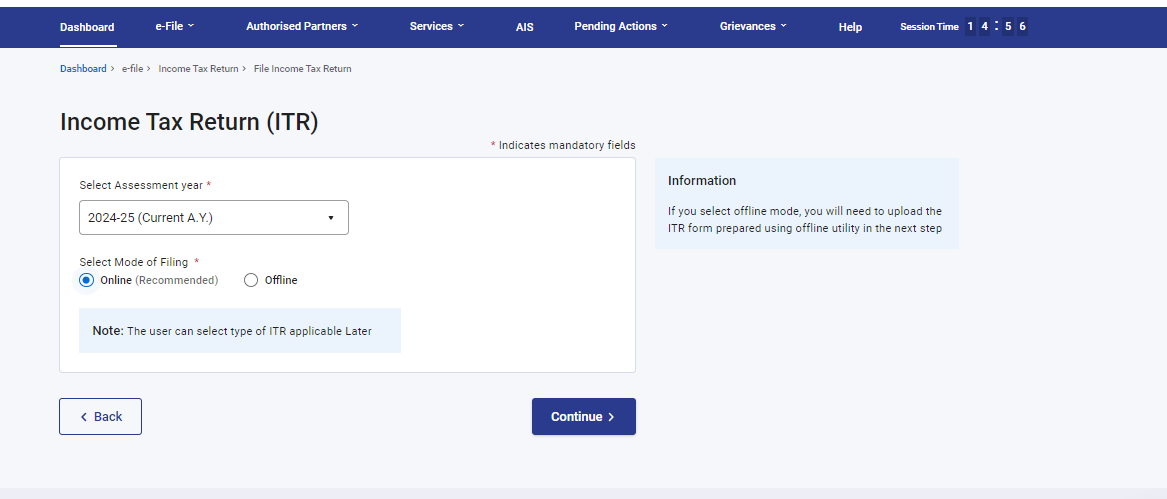

If filing for FY 2023-24 choose Assessment Year as AY 2024-25 or AY 2023-24 for FY 2022-23. Select mode of filing as Online and the filing type as original return or revised return. Original is when you’ve filed your ITRs on time and revised is when you make changes and file your ITR with corrections.

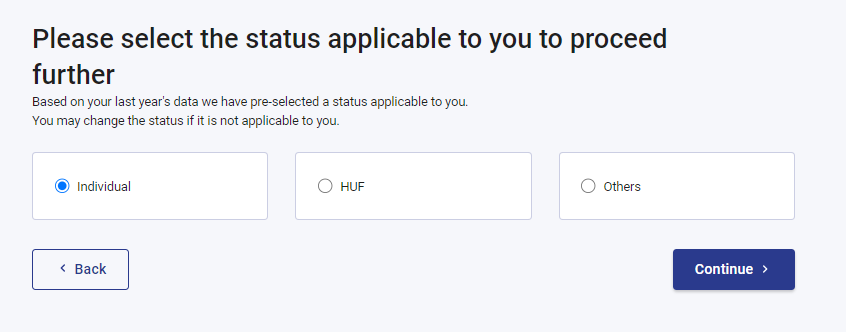

Select your applicable filing status: Individual, HUF, or Others.

Usually it is individual unless the tax filer has opted for another category.Select the relevant status and click on Continue.

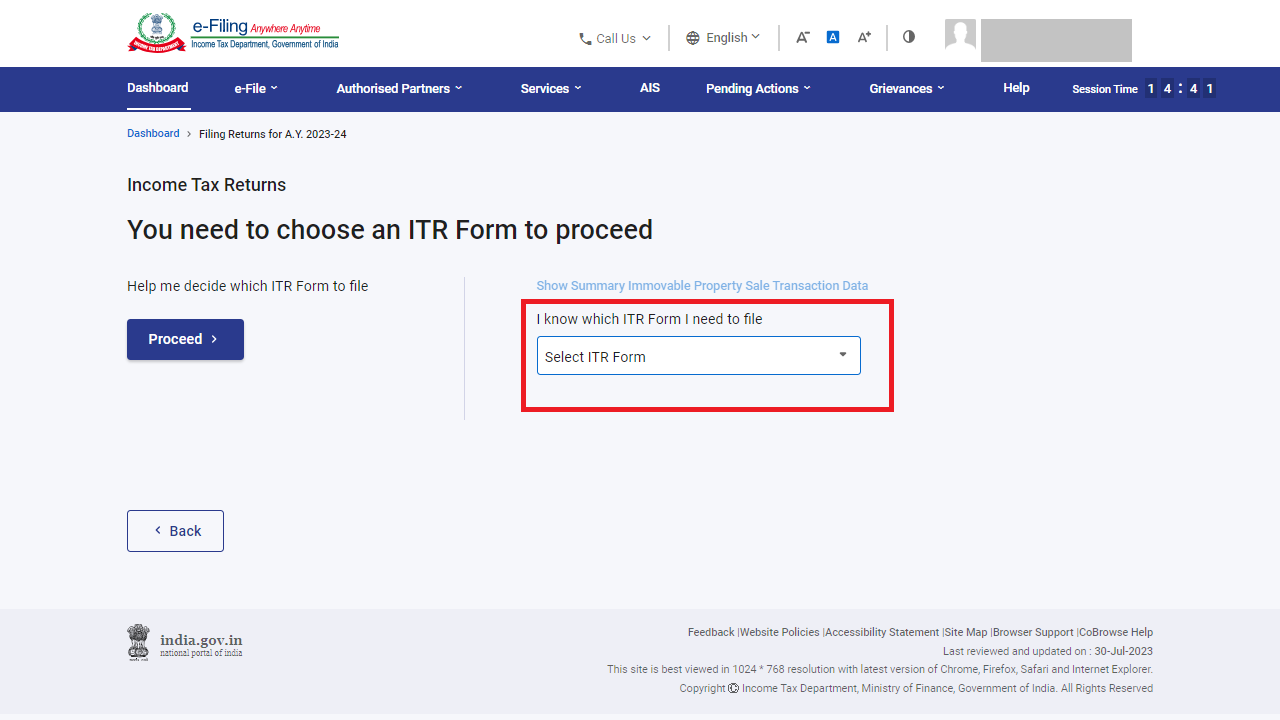

Now, select ITR type. There are a total of 7 ITR forms available, of which ITR 1 to 4 is applicable for Individuals and HUFs.

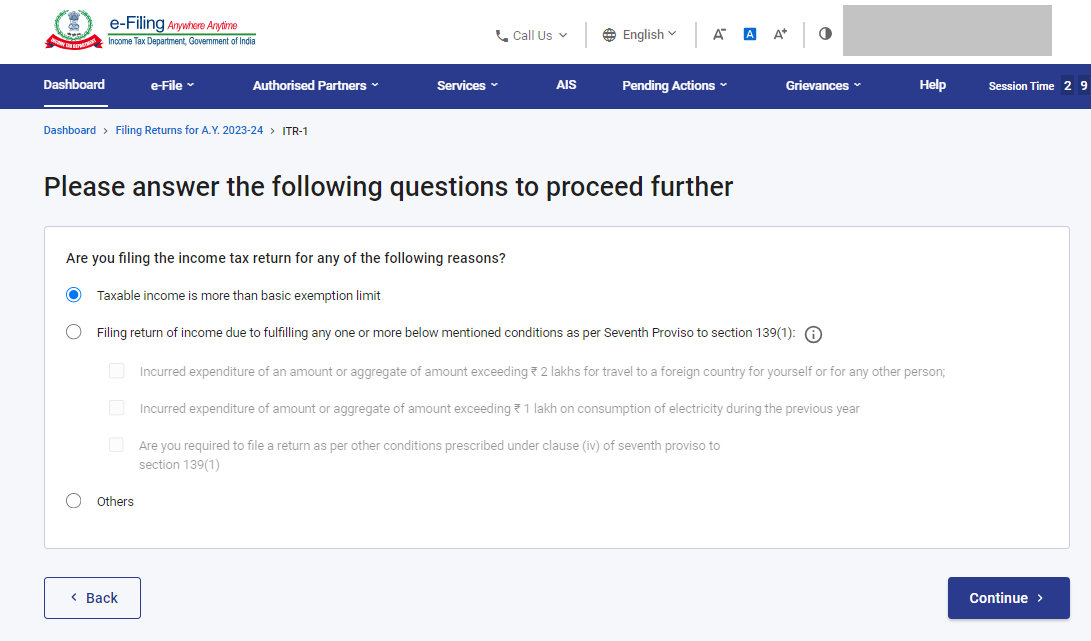

Step 6: Select your Reason For filing ITR

Select the option applicable to your reason:

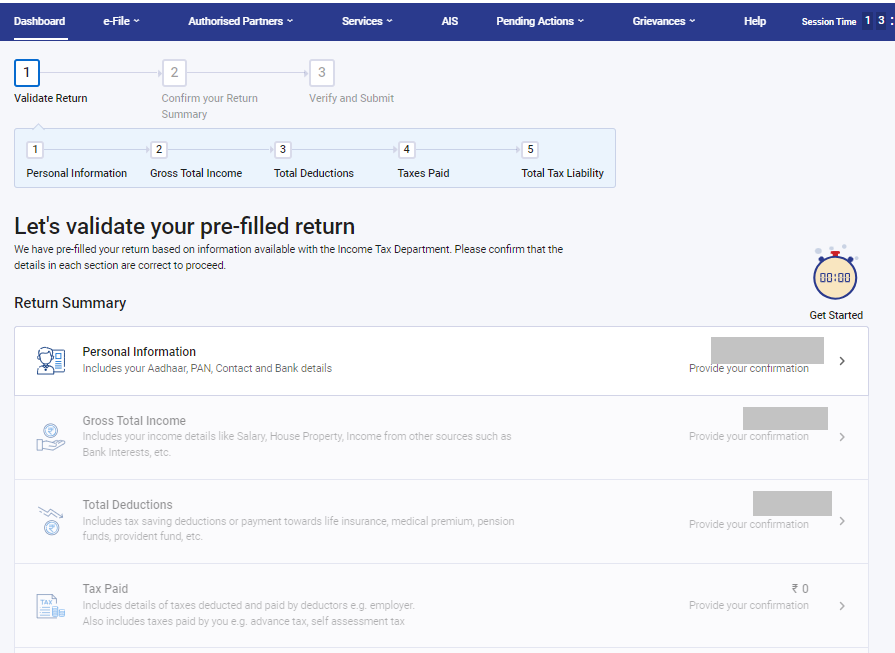

Validate your PAN, Aadhaar, Name, DOB, contact information, and bank details, that will be pre-filled, before you proceed further.

Disclose all relevant income, exemptions, and deduction details. Most of your details will be pre-filled based on the data provided by your employer, bank, etc. Review all the details before you proceed.

e-Verify your ITR using Aadhaar OTP, electronic verification code (EVC), net banking or by posting the physical copy of your ITR to CPC, Bengaluru within the time limit of 30 days.

What documents do I need to file my ITR?

Form 16: It is provided by your employer and contains details of the salary paid by them to you and the Tax deducted at source (TDS) on it.

Form 16A: It contains details on TDS deducted on interest received from deposits such as fixed or recurring bank deposits.

Form 16B: If you sell a property, TDS applies on the amount received from you by the buyer, the details of which are present in this form.

Form 16C: TDS details of the rent paid by your tenant to you are recorded here.

Form 26AS: This form represents your comprehensive statement of taxes against the PAN number. It includes TDS by your employer, bank or any other organization that has made a payment to you. Advance taxes or self-assessment taxes paid, proof of tax saving investments such as deductions as prescribed from Section 80C to 80U including life insurance policy or a term plan are also listed.

Other than the above you need to have:

Bank/Post Office Interest Certificates:

Provide break up of interest earned from post office savings accounts, savings bank accounts, recurring deposits and fixed deposits or any other source, as these are taxable.

Annual Information Statement (AIS):

The Annual Information Statement (AIS) is a more detailed document compared to the Form 26AS, as it includes all details of your financial transactions in a financial year.

Proof of Investment and Expenditure:

Provide your deposit certificates, demat account statements, investment receipts, etc., as investment and expenditure proofs.

Capital Gains:

Have made a profit of more than Rs.1 lakhs through your investments in shares, mutual funds debentures and property in a financial year? Then it is taxable under Long Term Capital Gains and for that you’d need to provide the relevant documents.

Details of Foreign Assets:

Disclose all the assets you hold in any foreign country, including bank accounts, property and so on in your ITR.

Aadhaar number:

As per Section 139AA of the Income-tax Act, 1961, it is mandatory to mention your Aadhaar card number in your ITR.

Bank Account Details:

Mention details of all the bank accounts you own, even if you have closed your account in the middle of the financial year.

In conclusion, filing your Income Tax Return (ITR) ensures compliance with tax laws, helps you claim refunds and deductions, and builds your credibility for future financial transactions. By understanding the process, keeping accurate records, and filing on time, you can avoid penalties and make the most of the benefits available. As tax laws evolve, staying informed and proactive about your ITR filing will serve you well, contributing to your overall financial well-being.

Disclaimer: The information in this article is compiled from various sources and is not to be taken as a substitute for professional advice on managing finances, reader discretion is advised.

.svg)

.svg)

axio (formerly known as Capital Float, Walnut & Walnut 369) is the brand name of CapFloat Financial Services Private Limited, an NBFC registered with the RBI.

© 2025 axio. All rights reserved